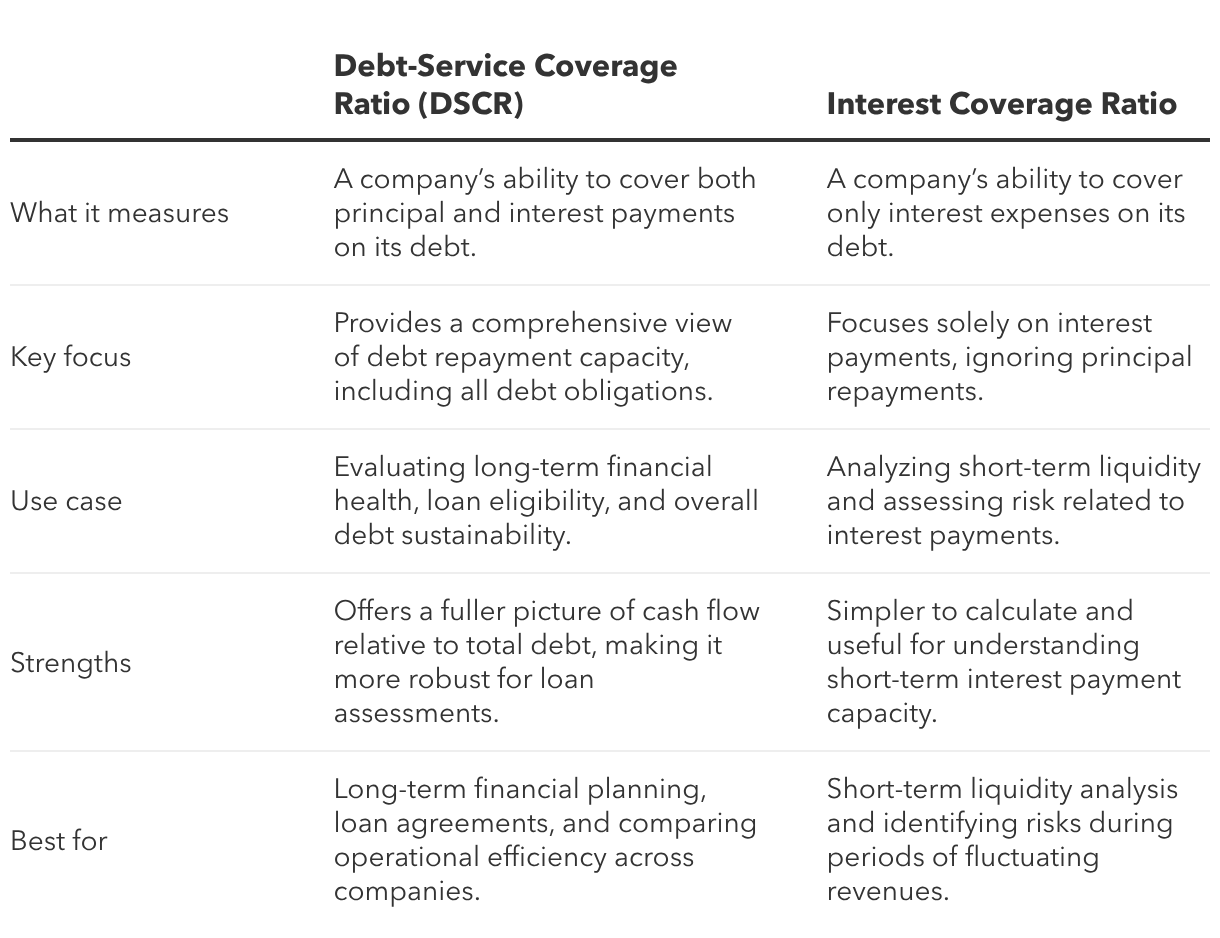

Breaking down the debt service coverage ratio (DSCR)

The debt service coverage ratio is a straightforward yet powerful metric for assessing a business’s ability to repay its debts. You can calculate it by dividing net operating income (NOI) by total debt service, which includes both principal and interest payments.

DSCR = Net Operating Income / Total Debt Service

This formula provides lenders and business owners with a clear picture of cash flow relative to debt obligations (or current liabilities).

To accurately calculate DSCR, you'll need to understand the two key components: net operating income and total debt service. Each plays a critical role in determining whether your business can comfortably meet its financial commitments. Let’s dive deeper into these terms and how to estimate them.

What counts as net operating income

Net operating income (NOI), the numerator in the debt service coverage ratio formula, represents the revenue left after covering operating expenses but before accounting for taxes and interest.

Nonoperating Expenses = Gross Operating Income - Operating Expenses

To calculate NOI, start with your total revenues and subtract operating expenses such as rent, utilities, payroll, and supplies. Exclude nonoperating costs like taxes, interest payments, or one-time expenses.

This metric focuses on core operations, providing a clear view of your business’s profitability while offering the necessary context you need to reduce operating costs.

Understanding total debt service

Total debt service, the denominator in the debt service coverage ratio, includes all scheduled payments due within a year, such as principal, interest, leases, and recurring debt expenses.

Special considerations like sinking funds or balloon payments may also factor in. Lenders analyze total debt service to assess financial obligations, helping evaluate your ability to manage debt and meet expectations.

Adjusting for taxes

For a more accurate debt service coverage ratio (DSCR) calculation, adjust for taxes on interest payments to reflect their tax-deductible nature. Since interest payments are typically tax-deductible, they reduce a company's taxable income, lowering the actual cost of the interest expense.

Factoring in this tax benefit allows for a more precise cash flow statement, which can help you assess your ability to pay off debts accurately.

This adjustment also ensures a clearer comparison across companies or industries with differing tax rates and offers a more realistic view of a business’s debt repayment capacity, helping lenders and stakeholders make informed decisions.